AI is transforming the world, and its effects are being noticed in all areas of life. AI is showcasing opportunities in all sectors of the economy and has the potential to revolutionise different industries. Like with the Dot-com bubble of the 2000s we don’t yet understand the full extent of what the future of AI holds, however one thing is sure to hold true, there is no going back. AI will be the future and economies that can take advantage of its potential are the ones that will stand the test of time. Just like the web revolutionised our lives and even till this day is still a core component of our lives, so will the advent of AI. In this post we will explore how AI is being funded, what countries are funding the most, and finally which industries are receiving these fundings. This in turn will help us understand how to position ourselves for the influx of AI and GenAI.

AI Economics

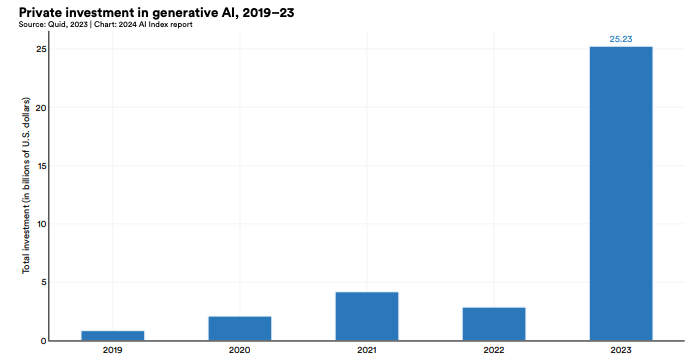

From data obtained by the AI index report, since 2021 corporate investment and private investment in AI have both been shrinking since 2021, however funding for generative AI (AI that can create its own contents across all mediums, think of ChatGPT) has been increasing at an astronomical rate. In 2022 the total investment in GenAI was 2.85 billion, which is dwarfed by the total investment in 2023 which scaled to 25.23 billion, a 885% increase, indicating businesses drive to harness GenAI (data). This doesn’t come as a surprise when we consider that ChatGPT came out in November 2022 and everyone and their grandmother could see the future altering potential that ChatGPT had unlocked.

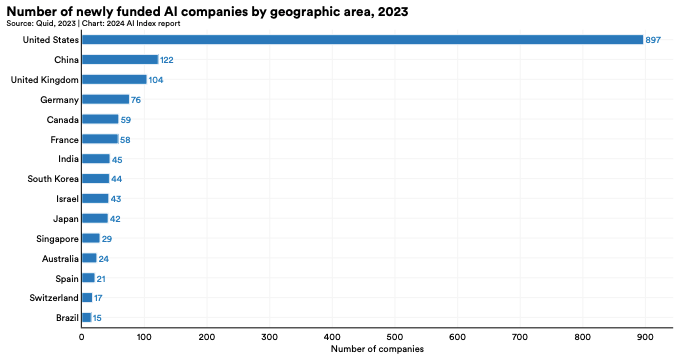

Focusing on GenAI, in 2023 there were 99 new Startups receiving funding, compared to 56 in 2022. As we know OpenAI changed the game making GenAI accessible to the mass market in 2022/2023 as it was still being developed (Figure 4.3.6 – Chapter 4.3 investment AI Index Report). Findings in the report showed that private investment in new Startups for GenAI has a huge regional disparity. The United States has outpaced the combined investments of China (0.65B) and EU & UK (0.74B) by approximately 21.07 billion (data). This is caused by the number of newly formed AI companies being predominately from the United States at a whopping 897 companies, and the next closest – China only at 122 and finally United Kingdom at 104. There is a clear disparity in how different countries are adopting the advancement of AI. The US has the infostructure and experience, thinking Google, Apple, Microsoft and more, who already have the base data infrastructure, data storage, chips for processing and technical skills to invest in smaller companies, whilst the UK is lagging behind in this department, however if we compare it to China who one might assume would be closer to the US, the UK is doing very well.

Next, we might ask ourselves what industries are actually taking advantage of these private investments which could potentially give us some insights as to what areas have the highest resources for easier transition into the field, or the potential of reducing the workforce.

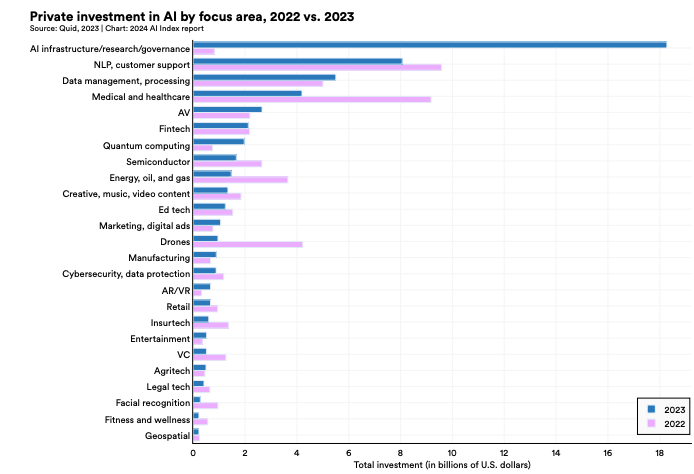

In 2022, AI infrastructure/research/governance had a total investment of 0.82 billion, however in 2023, there was a a huge surge in total investment in this sector to 18.27 billion, more than 20x the total investment of the previous year (data). The prominence of this surge can be reflected by the large investment in companies building AI applications such as OpenAI, Anthropic and inflection AI.

NLP and customer support, Medical and healthcare, Energy, oil and gas , drones, showed a major decline in AI investment in 2023, this could be caused by a number of factors. Let’s start with NLP and customer support, as we know there as been a shift to emerging AI technologies like GenAI which uses NLP and has better functionality for customer support. Another case is that NLP has now become standardised and incorporated into larger systems. For Medical and healthcare, there might be a pushback from market maturity and the area of focus for investments has changed since most processes within the medical and healthcare field have already reached their current peak stages for new funding, hence the huge drop in investment from 9.18 billion in 2022 to 4.2 billion in 2023 (data).

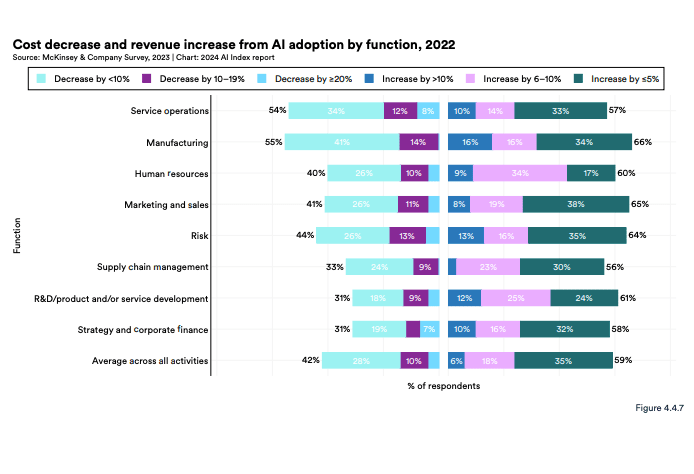

Let us now look at how cooperation’s are benefiting from the use of AI. From a report produced by Mckinsey & company survey in 2023 (collecting the cost decrease and revenue increase from AI adoption in 2022), it is found that manufacturing has had the biggest cost saving of 55%, followed by service operations at 54% then finally risk at 44%. For revenue gains the sector that benefited the the most were manufacturing at 66%, R&D at 61% although, R&D had the joint lowest cost decrease of 31% indicating that the R&D research was still unaffected by AI as much as other functions. In the case of manufacturing, according to monstarlab, AI has been effectively imbedded in a number of areas, ranging from manufacturing automation, supply chain and manufacturing control, to utilising data for pivotal business decisions. AI is touching all aspects of manufacturing that were very difficult in the past and helping it speed up its processes, in return, cutting costs and increasing production rate hence revenue increase.

Next lets look at how AI talents are moving across the board, below we notice that Luxembourg, Switzerland , and UAE have the highest influx of AI talent, in contrast, the UK has a declining AI talent, indicating more AI talents are flowing out than coming in. Switzerland appeals to AI professionals due to its strong support in both public and private sector partnerships making it an attractive destination, the quality of life for both Luxembourg and Switzerland is also a key point to the influx of talent. Next we have UAE which is diverging from its original model of oil and gas to finance and tech. It also offers 0 tax further incentivising AI talents to move to the UAE. Personally there is no surprise that the UK is so low, from the high taxes, the very high competitive nature of the space, companies prefer cheaper labour so they outsource a lot of work to developing countries, and the overall quality of life has been decreasing. This was reinforced by the happy index placing the UK 20th in the world, where we compare Luxembourg and Switzerland at 8 and 9th respectively.

Conclusion

AI is transforming the world, revolutionizing industries and creating unprecedented opportunities much like the web did decades ago. Despite a decline in overall AI investment since 2021, funding for generative AI has surged dramatically, driven by innovations such as ChatGPT. The United States leads in AI investment, significantly outpacing other regions due to its robust technological infrastructure. Sector-wise, investments are shifting towards AI infrastructure and research, with notable declines in areas like NLP and healthcare. Corporations, particularly in manufacturing, are seeing substantial cost savings and revenue gains from AI adoption. Countries like Luxembourg, Switzerland, and UAE are attracting top AI talent, while the UK faces a talent drain. Understanding and adapting to these trends will be crucial for thriving in the AI-driven future.

Full report: https://aiindex.stanford.edu/report/